Fintech Companies London: Top 10 Leading Firms

![]() • October 25, 2025

• October 25, 2025

London stands as one of the world’s most influential financial centres, and in recent years, it has evolved into a leading hub for fintech innovation.

The convergence of finance and technology has created a thriving industry where startups, scaleups and established financial institutions collaborate to reshape the way financial services are delivered.

The UK’s fintech sector contributed £11 billion to the economy in 2023 alone, according to Innovate Finance, with London at the heart of this growth. Home to more than 2,500 fintech firms, London offers a rich ecosystem of investors, talent, and regulators, making it a magnet for innovation.

This article explores ten of the most prominent fintech companies in London that are shaping the future of financial technology both nationally and globally.

Why London is the Epicentre of Fintech Startups?

London’s position as a top destination for fintech innovation is built on a solid foundation of capital access, regulatory frameworks, and world-class talent.

Access to Capital and Investment

London is consistently ranked among the top global cities for venture capital investment in fintech. This funding environment enables startups to scale rapidly.

- Over £4 billion was raised by UK fintechs in 2022

- Major investors include Index Ventures, Accel, and Balderton Capital

- Multiple government-led initiatives encourage fintech innovation

Regulatory Support and Innovation

The UK’s Financial Conduct Authority (FCA) actively supports fintech development through forward-thinking policies.

- The FCA sandbox allows fintechs to test services in a controlled environment

- The UK Government’s Kalifa Review promotes long-term sector growth

- Fast-track licensing and open banking standards encourage competition

Skilled Workforce and Talent Pool

London has access to a rich blend of financial and technical professionals. This is bolstered by its proximity to universities such as Imperial College London, UCL, and LSE.

- More than 60% of UK fintech jobs are based in London

- Access to international talent through flexible visa routes

- Cross-functional skills in coding, data analysis, and finance

Proximity to Financial Institutions

London is home to over 250 foreign banks and numerous global headquarters. This creates opportunities for B2B partnerships, collaborations, and enterprise-level innovation.

- Fintechs benefit from close ties with established financial institutions

- Large banks serve as early adopters and innovation partners

- Hybrid models between banks and fintechs are becoming more common

Top 10 Fintech Companies in London

1. Revolut

Revolut has become one of the most recognisable names in the global fintech sector since its launch in London in 2015. What started as a low-cost foreign exchange card has transformed into a comprehensive financial super app, offering a broad range of services including banking, investing, cryptocurrency, budgeting, and insurance.

The company was founded by Nikolay Storonsky and Vlad Yatsenko with a mission to eliminate hidden banking fees and make global spending more accessible. As of 2025, Revolut operates in more than 35 countries and continues to expand aggressively into both developed and emerging markets.

Its competitive advantage lies in its all-in-one approach, allowing users to manage their entire financial life through one mobile app. With advanced budgeting tools, investment opportunities in crypto and stocks, and even travel perks like airport lounge access, Revolut has positioned itself as the go-to digital financial solution for individuals and businesses alike.

Revolut Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2015 |

| Founders | Nikolay Storonsky, Vlad Yatsenko |

| Headquarters | London, UK |

| Key Services | Banking, crypto, stock trading, budgeting tools, business accounts |

| Users (2025) | Over 35 million personal users, 500,000+ businesses |

| Unique Feature | All-in-one financial super app with international coverage |

| Global Presence | Operations in 35+ countries |

| Revenue Model | Subscription tiers, interchange fees, FX margins, lending |

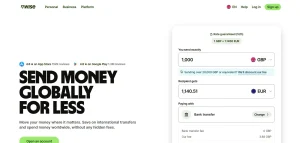

2. Wise (formerly TransferWise)

Wise was launched in 2011 by Estonian entrepreneurs Taavet Hinrikus and Kristo Käärmann with the aim of making international money transfers faster, cheaper, and more transparent. The founders themselves were frustrated by the hidden fees and poor exchange rates offered by traditional banks, and built a peer-to-peer system that bypassed those costs.

Wise allows users to send and receive money across more than 160 countries, all while using the real exchange rate. Its multi-currency account enables individuals and businesses to hold, convert, and spend in over 50 currencies, making it a favourite among freelancers, SMEs, and global nomads.

The company went public in 2021 on the London Stock Exchange via a direct listing and has since expanded its services to include borderless banking and international payroll services.

What sets Wise apart is its relentless focus on transparency and efficiency. The platform offers clear breakdowns of fees, and its pricing structure is consistently among the lowest in the industry.

Wise Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2011 |

| Founders | Taavet Hinrikus, Kristo Käärmann |

| Headquarters | London, UK |

| Key Services | Cross-border money transfers, multi-currency accounts, borderless cards |

| Users (2025) | Over 16 million customers worldwide |

| Unique Feature | Real exchange rate with no hidden fees |

| Global Reach | 160+ countries, 50+ currencies supported |

| Revenue Model | Transaction fees, business services, subscriptions |

3. Monzo

Monzo is one of the UK’s most popular digital-only banks, known for its user-friendly interface and transparent business model. Founded in 2015 by Tom Blomfield and a team of former bankers and developers, Monzo quickly gained a reputation for customer-focused innovation.

It started by offering pre-paid debit cards linked to a mobile app and later obtained a full UK banking licence in 2017. Monzo’s current account features tools that help users manage their finances with ease, including real-time spending notifications, savings pots, bill splitting, and budgeting categories.

What differentiates Monzo is its community-driven approach to product development. The company regularly incorporates customer feedback and even publishes detailed updates about upcoming features.

In addition to personal accounts, Monzo has expanded its offerings to include business banking, loans, and investment options. It continues to focus on the UK market but has hinted at future international expansions.

Monzo Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2015 |

| Founder | Tom Blomfield and co-founders |

| Headquarters | London, UK |

| Key Services | Digital current accounts, savings, budgeting tools, loans, business banking |

| Users (2025) | Over 8 million customers in the UK |

| Unique Feature | Real-time insights and community-led development |

| Business Services | SME accounts, invoicing, accounting integrations |

| Revenue Model | Interchange fees, premium accounts, lending, interest on deposits |

4. Starling Bank

Starling Bank is one of the most successful challenger banks in the UK, known for offering a full suite of digital banking services for both personal and business customers.

Founded in 2014 by Anne Boden, a former banking executive, Starling was among the first app-based banks in the UK to receive a full banking licence from the Prudential Regulation Authority.

Unlike some fintechs that operate under an e-money licence, Starling is a fully licensed and regulated bank. It provides current accounts, overdrafts, loans, and savings products, all accessible through a slick mobile interface.

The bank has gained popularity for its intuitive features such as real-time payment notifications, integrated budgeting tools, and card controls.

What sets Starling apart is its strong focus on business banking. It offers SME accounts with built-in tools for expense management, invoicing, and VAT tracking. The bank is also known for its commitment to profitability, a rare trait among challenger banks.

Starling Bank Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2014 |

| Founder | Anne Boden |

| Headquarters | London, UK |

| Key Services | Current accounts, overdrafts, business banking, personal loans |

| Users (2025) | Over 4 million retail users and 500,000+ business accounts |

| Unique Feature | Full banking licence with strong SME offering |

| Awards | Best British Bank (multiple years) |

| Revenue Model | Lending interest, interchange, business fees |

5. Checkout.com

Checkout.com is a global payment processing company that provides end-to-end digital payment solutions for online businesses. Founded in 2012 by Guillaume Pousaz, the company has grown rapidly to become one of Europe’s highest-valued fintech firms, with a valuation exceeding $40 billion at its peak.

Checkout.com specialises in enterprise-grade payment infrastructure and works with some of the world’s largest brands, including Netflix, Pizza Hut, and Klarna. Its platform supports payments in over 150 currencies and offers services such as fraud prevention, real-time authorisations, and advanced analytics.

The company distinguishes itself with a modern, modular API that gives merchants granular control over the checkout experience. This allows clients to tailor payment flows and optimise transaction performance across geographies.

Checkout.com continues to invest heavily in research and development, particularly in areas like embedded finance and data-driven payments optimisation.

Checkout.com Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2012 |

| Founder | Guillaume Pousaz |

| Headquarters | London, UK |

| Key Services | Online payment processing, fraud prevention, payment analytics |

| Clients | Netflix, Farfetch, Klarna, Sony |

| Currencies Supported | Over 150 |

| Unique Feature | Modular API for full customisation and real-time authorisations |

| Revenue Model | Transaction fees, enterprise services, platform usage |

6. Zopa

Zopa is one of the UK’s oldest fintech pioneers. Originally launched in 2005 as the world’s first peer-to-peer (P2P) lending platform, Zopa allowed individual lenders to connect directly with borrowers, disrupting the traditional lending model.

In 2020, Zopa transitioned from a P2P platform to a fully licensed digital bank after acquiring a banking licence from the Bank of England. This strategic move allowed the company to offer new products including personal loans, credit cards, and fixed-term savings accounts.

Zopa focuses on responsible lending, supported by its proprietary credit risk technology. It evaluates a wide range of financial behaviours to determine eligibility, helping to reduce default rates and improve customer outcomes.

Its banking app is simple, user-friendly, and tailored for users seeking transparency and control over their finances. Zopa has also expanded into auto financing and continues to explore additional lending verticals.

Zopa Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2005 (as P2P platform), 2020 (as digital bank) |

| Headquarters | London, UK |

| Key Services | Personal loans, credit cards, fixed-term savings, auto finance |

| Users (2025) | Over 1 million active users |

| Unique Feature | Credit risk modelling with focus on responsible lending |

| Notable Shift | From P2P lending to licensed digital banking |

| Revenue Model | Interest income, card fees, savings spread |

7. Curve

Curve is a London-based fintech that brings a unique approach to personal finance management. Instead of launching a new bank or payment account, Curve acts as a smart payment aggregator, allowing users to consolidate all their debit and credit cards into one physical card and mobile app.

Founded in 2015 by Shachar Bialick, Curve’s innovation lies in its ability to streamline payment management without requiring users to switch banks. Users can spend from any linked account, track their expenses in real time, and even retroactively change which card a purchase was made on using its signature “Go Back in Time” feature.

Curve also offers rewards and cashback programmes, real-time spend notifications, and travel perks such as fee-free foreign exchange. The app includes budgeting tools and spend categorisation, appealing to users seeking convenience and financial clarity.

In recent years, Curve has expanded to offer buy-now-pay-later (BNPL) options and launched a credit feature called Curve Flex. It continues to grow its European presence and is exploring expansion in the US.

Curve Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2015 |

| Founder | Shachar Bialick |

| Headquarters | London, UK |

| Key Services | Card aggregation, expense tracking, BNPL, smart payments |

| Users (2025) | Over 4 million across the UK and Europe |

| Unique Feature | Go Back in Time" to switch payment cards post-transaction |

| Integrated Cards | Visa, Mastercard, AMEX (in beta) |

| Revenue Model | Interchange fees, premium subscriptions, BNPL lending |

8. OakNorth

OakNorth is a commercial bank focused exclusively on the UK’s scale-up and mid-sized business sector—a demographic often underserved by traditional banks. Co-founded in 2015 by Rishi Khosla and Joel Perlman, OakNorth combines data-driven credit analysis with deep sector expertise to provide customised lending solutions.

The bank’s proprietary platform, the OakNorth Credit Intelligence Suite, uses machine learning and structured data analysis to assess credit risk, enabling faster, more accurate lending decisions. This allows OakNorth to support businesses with flexible loans ranging from £500,000 to £25 million.

OakNorth positions itself between high-street banks and alternative lenders, offering both the capital and speed needed for growing firms. Its portfolio includes companies in sectors like hospitality, healthcare, property development, and manufacturing.

OakNorth Bank operates under a full banking licence and also licenses its credit technology to banks in international markets, generating additional revenue streams through software-as-a-service (SaaS).

OakNorth Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2015 |

| Founders | Rishi Khosla, Joel Perlman |

| Headquarters | London, UK |

| Key Services | SME loans, commercial banking, credit analysis software |

| Clients (2025) | Over 5,000 mid-sized UK businesses |

| Unique Feature | Credit Intelligence Suite for data-driven lending |

| Loan Range | £500,000 to £25 million |

| Revenue Model | Interest income, SaaS licensing, loan structuring fees |

9. ClearBank

ClearBank is a clearing and embedded banking infrastructure provider that supports other fintechs, neobanks, and financial institutions with modern payment and settlement solutions. Founded in 2015 by Nick Ogden, it is the first new clearing bank in the UK in over 250 years.

Rather than serving end consumers directly, ClearBank provides banking-as-a-service (BaaS) and API-driven infrastructure to fintech companies. This enables real-time payments, faster settlements, and full access to UK payment schemes including BACS, CHAPS, and Faster Payments.

One of ClearBank’s most prominent partners is Tide, the SME banking platform. Through its services, Tide can offer current accounts, savings, and lending without needing its own banking licence. ClearBank is also FCA-regulated and holds customer deposits at the Bank of England, ensuring security and trust.

With the growing demand for embedded finance and open banking, ClearBank is strategically positioned to become the backbone of digital banking infrastructure across Europe and beyond.

ClearBank Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2015 |

| Founder | Nick Ogden |

| Headquarters | London, UK |

| Key Services | Clearing, settlement, banking infrastructure, BaaS |

| Clients | Tide, Raisin, and multiple fintech platforms |

| Unique Feature | Real-time access to UK payment schemes via cloud infrastructure |

| Regulation | FCA-regulated, deposits held at Bank of England |

| Revenue Model | Platform access fees, infrastructure-as-a-service |

10. Thought Machine

Thought Machine is a fintech scale-up that specialises in core banking technology. Founded in 2014 by Paul Taylor, a former Google engineer, the company aims to modernise the outdated legacy systems used by traditional banks with its cloud-native platform, Vault Core.

Vault Core allows banks to create, deploy, and manage financial products at scale, including current accounts, loans, savings, and credit. Unlike legacy systems, Vault is built using smart contracts, enabling complete flexibility and product customisation.

Thought Machine’s technology has been adopted by major banks including Lloyds Banking Group, Atom Bank, and Standard Chartered.

The company has expanded internationally with offices in Singapore, New York, and Sydney, and is working with Tier 1 banks to support digital transformation globally.

Its modular architecture, API-first design, and scalability make it a preferred solution for both traditional banks and new digital entrants.

Thought Machine Company Snapshot

| Attribute | Details |

|---|---|

| Founded | 2014 |

| Founder | Paul Taylor |

| Headquarters | London, UK |

| Key Services | Core banking systems, smart contracts, product customisation |

| Clients | Lloyds, Atom Bank, Intesa Sanpaolo, SEB |

| Unique Feature | Cloud-native Vault Core platform with smart contract flexibility |

| Global Reach | Operations in the UK, US, Europe, and APAC |

| Revenue Model | Enterprise licensing, implementation services, cloud hosting fees |

What Sets These Fintech Firms Apart?

These companies stand out for their innovation, customer focus, and adaptability to technological change.

Common Strengths:

- Advanced use of APIs, machine learning, and cloud infrastructure

- Frictionless user experiences through mobile-first design

- Scalable platforms catering to individuals, SMEs, and large enterprises

- Rapid market entry and product iteration cycles

Key Features of Top Fintechs:

| Company | Core Offering | Unique Strength |

| Revolut | Multi-service financial app | Wide global presence and crypto trading |

| Wise | Cross-border money transfer | Transparent pricing with mid-market rates |

| Monzo | Mobile banking | Instant alerts and intuitive budgeting |

| Starling Bank | Personal & business banking | In-app accounting for businesses |

| Checkout.com | Online payment processing | High scalability and enterprise support |

| Zopa | Digital loans & savings | Credit optimisation tools |

| Curve | Card aggregator | Transaction modification features |

| OakNorth | SME lending | Data-driven credit modelling |

| ClearBank | Real-time clearing bank | Cloud-native API-based infrastructure |

| Thought Machine | Core banking tech | Flexible product creation via smart contracts |

What is the London’s Fintech Ecosystem and Future Growth?

The fintech ecosystem in London benefits from close-knit collaboration between private firms, public organisations, and academic institutions.

Innovation Hubs and Accelerators

London hosts multiple fintech accelerators, including:

- Level39 at Canary Wharf

- Barclays Rise

- Techstars London

These hubs provide early-stage companies with mentoring, investment access, and office space.

Emerging Trends

Several forward-looking trends are shaping the next wave of fintech growth in the capital:

- Open banking and data-driven personal finance solutions

- Embedded finance services across retail and e-commerce platforms

- ESG-focused fintechs helping users track carbon footprint and green investments

Talent and Education

Initiatives such as the Fintech Pledge aim to bridge skills gaps in the sector. Partnerships with universities like King’s College London and the University of Cambridge foster academic-industry collaboration in AI, finance, and cybersecurity.

Government and Policy Support

Ongoing support from UK government initiatives helps maintain London’s competitive edge:

- The Kalifa Review outlines national fintech strategy

- Tax incentives such as SEIS and EIS attract investment

- Flexible regulatory frameworks for innovation in crypto, regtech, and payments

Conclusion

London’s fintech scene is not just thriving; it’s evolving at a pace that few other cities can match. The synergy between startups, financial institutions, regulators, and investors continues to fuel growth.

As new technologies and business models emerge, these top fintech companies are set to redefine financial services across the UK and beyond.

With strong institutional support, talent availability, and access to capital, London will remain at the forefront of fintech innovation for years to come.

Frequently Asked Questions

What is the fastest-growing fintech company in London?

Revolut is often cited as the fastest-growing due to its rapid international expansion and diversified financial services.

How do fintech companies in London get regulated?

They are primarily regulated by the Financial Conduct Authority (FCA) which oversees compliance, consumer protection, and financial conduct.

What makes London attractive for fintech startups?

London offers access to funding, a skilled workforce, supportive regulation, and proximity to global financial markets.

Are there funding opportunities for fintechs in the UK?

Yes, numerous venture capital firms, government grants, and accelerator programmes provide funding for fintech startups.

What sectors are London fintech companies disrupting?

They are disrupting sectors like payments, lending, wealth management, insurance, and core banking.

Which fintech companies are hiring in London now?

Many, including Wise, Starling Bank, Thought Machine, and Checkout.com, have active recruitment programmes.

How can someone start a fintech business in the UK?

Starting a fintech in the UK requires a clear business model, FCA approval (if needed), funding, and adherence to regulatory standards.